Framing operators are informed of the rate floor and the number of numbers, and the broker will comply with it, as he went half way correct. At times, brokers value it. Occasionally, they take the place of the truck. Both occur frequently enough to make it impossible to formulate a rule.

Wednesday morning. A broker that the operator has been working with for 9 months calls with a 580-mile load. The quoted rate is $200 below the operator’s floor rate for that lane. Three other carriers are interested, and the broker says he needs the response in “the next half hour”. The operator has about ninety seconds to decide on how to proceed on the call before the conversation is either a yes or the broker’s next call.

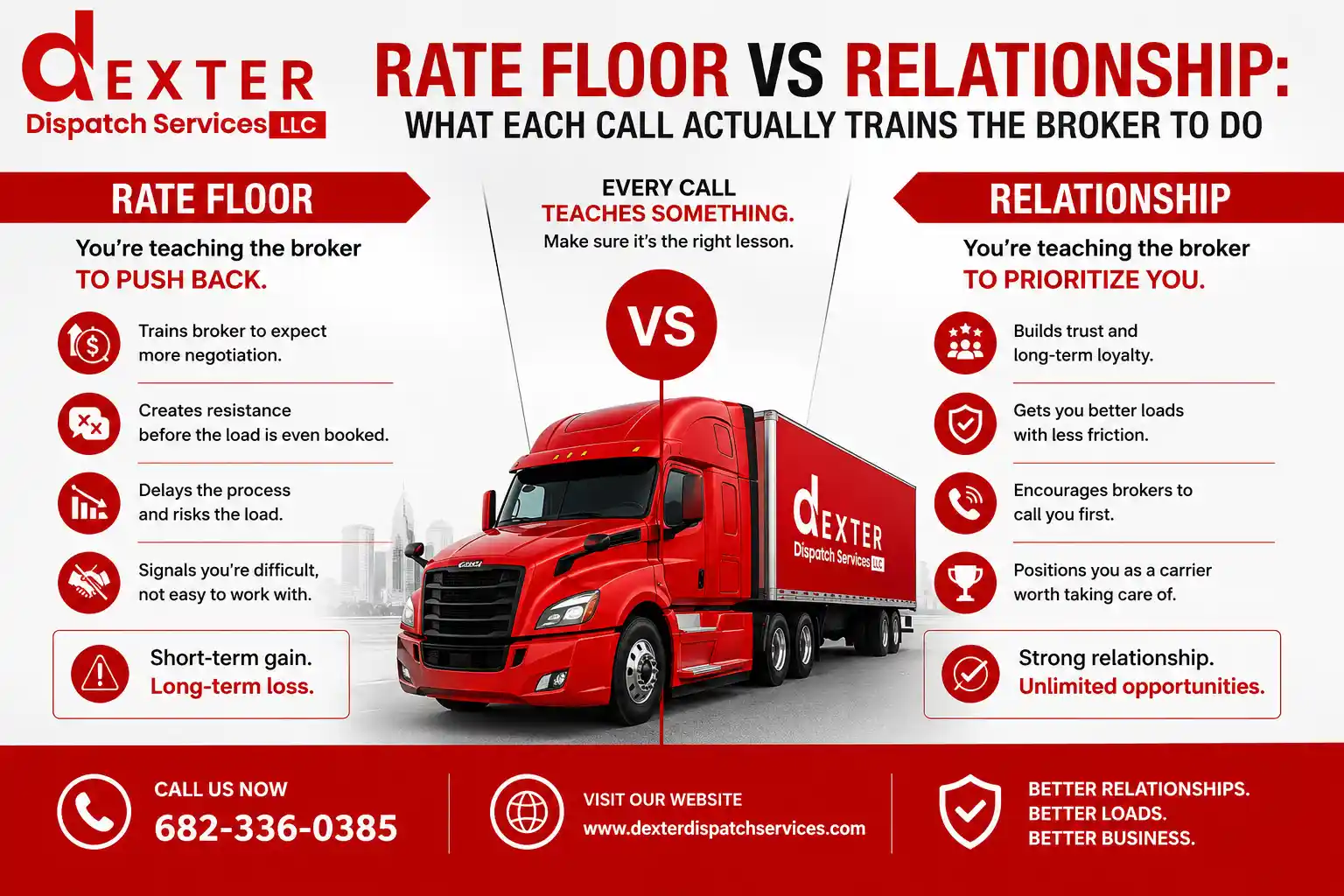

Whatever the operator says, trains the broker! This is something most advice on rate discipline fails to mention. Holding the floor will teach the broker that the operator’s number is legit. If the broker can take the load, then that is training for him that the operator number is soft. Both are types of training. They make various brokers in 9 months.

What holding the floor actually does

The operator replies: No. On the broker’s end, there is a half-second delay. The broker will sometimes say, Let me check with my customer,” and call back 20 minutes later with the rate changed. A broker can say, “Okay, I’ll remember you,” in a more flattering tone than when they first called you and may cut the call short. Both are so common that the operator can’t be certain that they will receive the same one the following week from the same broker.

In the absence of the broker’s return, the load is delivered to another carrier. The operator is sitting without freight on Wednesday afternoon, and the thing the part operators often overlook is what happens on the next load—the order the broker will run their list. The carrier that had the floor shifts one or two slots down the queue. As long as it’s not first, it’s still called. When that change happens over a quarter, it results in fewer initial looks, which, in turn, makes the lane quieter and lacking a point to look at.

The broker is not lost if they hold the floor. It merely alters the broker’s operating procedures. The thinner the load board, the quicker the broker will return and will keep the carrier towards the top of the board. A broker that has regular volume generally will not. On most days, the operator is unaware whether they are working with a broker or not.

What taking the load actually does

The operator responds: “Yes”. You load your truck, go down the lane, and are paid the lesser rate. Revenue from the week is saved. The relationship continues. The operator exudes the image of a carrier better able to solve the broker’s problem when one exists.

The training that occurs is more subdued. Two weeks later, another load, at the same broker, is called, again under margin. The call goes through more quickly, there’s less pre-negotiation delay, there are fewer “let me see what I can do” pauses, and the opening rate is closer to the broker’s target. Previous broker call stored in broker’s file: This carrier’s call moved on test. The negotiation script is modified.

It’s a proven fact that operators who routinely accept loads below the floor track to this same pattern six months later—that, in turn, is how rates are trending from two to three per cent. Because the broker has gained first-hand knowledge that this passenger carrier wouldn’t need the “I’ll check with my customer” callbacks, they occur less frequently. The process of negotiating shortens or abridges. From inside the truck, it seems like regular market fluctuation. It isn’t.

The broker’s side of the same call

Rate floors aren’t a morality test at every broker. They’re shooting the cows for themselves. Shipper has a budget designated. The broker’s margin must be covered. The load must be moved on a date. The broker is tuning to (fact is all the carriers) and measuring against each of them.

If a broker is desperate to get the load off his hands, he will move on the rate. Three carriers calling a broker won’t. Before the call, a dispatch desk will read what side the broker is on. An understanding broker will remember that the carrier said no one had a rough week. Each broker who is measured during that quarter will recall the carrier said, “yes,” when “no” was being tossed around. All of those brokers are correct. They’re running on different incentives, and typically, the operator can’t tell which incentive is in use for any particular call.

This is some of what makes the rate-floor question not a rule. The operator is deciding on a particular call. The other end broker decides on a given load. If those two decisions do not dovetail together, much of it is a matter beyond the operator’s control.

If rate floor calls are still coming out in the same fashion and the lane access is still going astray, then walk/walk trade the pattern with a desk that monitors both sides of the trade.

Where the decision isn’t actually a decision

Not all rate-floor calls are rate-FDD tradeoffs. The operator is sitting empty in a yard with no other freight in sight. The. The truck is going to deadhead 200 miles to load somewhere else, or the freight that is $200 under the floor still nets better than running empty. The injection of math determines which option it is. There is no relationship-pricing question to answer, as the other option is worse.

Other calls aren’t tradeoffs either, in the other direction. The operator is in a tight market, has three load options on the board, and the broker under the floor is not competitive with the alternatives. It’s easy for the operator to say no, since there is no real cost.

Those that are in the middle are the hard calls—the ones operators debate with one another. It’s good to have a little freight, but it’s not “Great” freight. The condition of the lane is neither good nor bad. The broker is OK, but the operator isn’t seeing the best of their relationship. All of the input is within a safe range, and the math doesn’t automatically make the choice. In a nutshell, it is an actual decision the operator faces between two posture training futures, each with its own costs.

The honest version

Operators that get the lion’s share of the weeks come out with lower broker counts and slightly higher average rates. Those who flex receive wider access to the brokers and a little less for it. They’re both legitimate businesses; neither is at fault. In markets with a floor, always taking the floor is good advice. The suggestion to maintain the relationship at all costs goes to markets where the broker commits to a reciprocal relationship at all times. It isn’t a moral call on Wednesday, rather, a posture call with two real costs, and an unclear payoff curve for most operators.

What dispatch can see that the operator alone can’t

It is not market data that the information operators typically lack on the rate-floor call. That is published by DAT/123Loadboard, and the low for operational costs is widely known. It’s a broker-side context. What is this broker’s week thin as a load board? Has this broker been trending higher or lower on this lane over the past month? Do the alternative carriers the broker mentioned compete, or is the broker positioning? It’s very difficult to understand that context from a single phone call.

For a broker running multiple operators, desk-side context is built up as a by-product as well: the operator who came back with the rate after a ‘no’, other operators who didn’t, which had a thinned board, which one was pricing tighter this quarter. None of it can ‘save’ the operator from the call. Having been sharpened into a clear picture of the price tag for each posture with this broker this week, this lane.

At the Wednesday call, it is the operator who makes the decision again. It is still unclear whether there is a rule that covers all versions of the call. It still costs for two things: trade. The difference is whether the operator is making a selection blind or with the broker’s pattern in front of them. The entire fee for a dispatched truck is not correlated with the call. It’s valued based on information available before the broker call.

👉 Contact Dexter Dispatch Services at www.dexterdispatchservices.com or call us at [682-336-0385]